Test Yourself

Sign up to access your free download and get new article notifications, exclusive offers and more.

Enterprise Value (EV)

September 22, 2020

What is Enterprise Value?

Enterprise value is one of the most common types of company valuation used in corporate finance, along with equity value. Enterprise value is the value of the operational business, independent of capital structure. Equity value (or market capitalization) is the value attributable to the owners or shareholders (frequently expressed on a per-share basis for public companies).

For valuation purposes, enterprise value focuses on the operations of the company and is unaffected by financing decisions (unlike equity value). When considering what drives its value, this includes company performance, industry dynamics and general economic factors. The distinction between enterprise value and equity value is important for analysts who want to ignore the impacts of capital structure. A company looking to acquire a target company is likely to be more interested in the sales, cost structure and products it sells. This is because companies looking to value and acquire a target can change the capital structure (how the company is financed) with ownership.

Key Learning Points

- Enterprise value is the value of the operational business and is unaffected by capital structure changes (except at high leverage levels where the level of debt confers extra risk as the default probability rises)

- It is driven by a combination of factors including company performance, industry dynamics and economic climates

- The EV to equity bridge is summarized as enterprise value = equity value + debt – cash and cash equivalents

- The enterprise value of a company should always be compared with comparable companies to provide meaningful outcomes i.e. operate in similar industries, similar depreciation policies

Calculating the Enterprise Value

In order to find the enterprise value we can expand and rearrange the accounting equation:

Assets = Liabilities + Equity

Since enterprise value is the fair value of the net operational assets, the equation can be expanded to identify these components as follows:

Operating Assets + Cash = Operating Liabilities + Debt + Equity

If the equation is rearranged, the operating components can be isolated:

Operating Assets – Operating Liabilities = Debt + Equity – Cash

Balance sheet amounts are book value or carrying value but for valuation, all components must be at the market or fair value. We assume that cash is excess cash and part of the capital structure. Debt less cash is known as net debt.

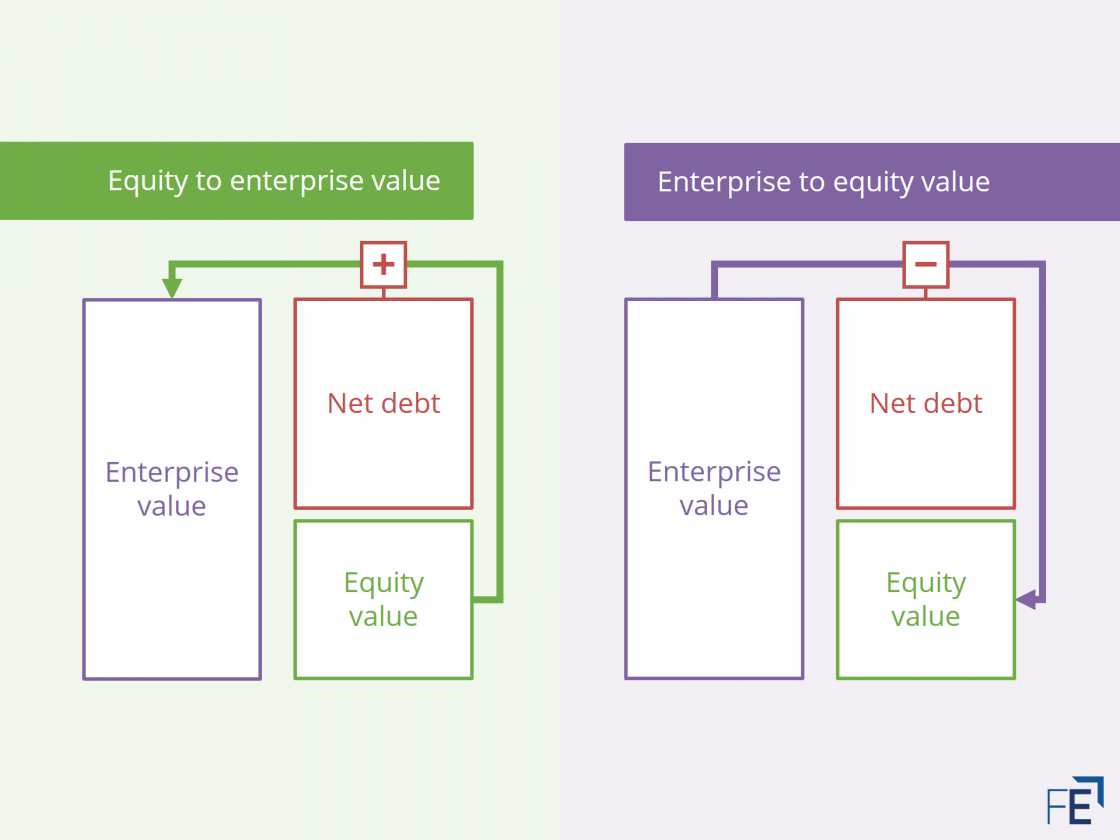

Enterprise to Equity Value Bridge

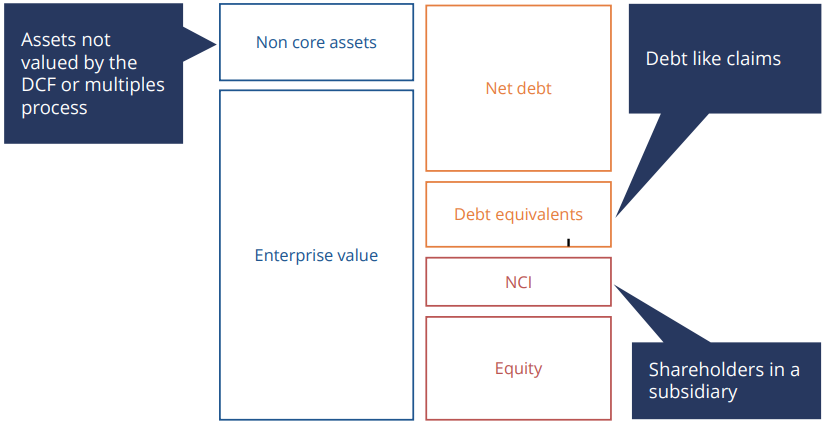

Since enterprise value equals net debt plus equity, the enterprise value can be derived from the equity value and vice versa. In addition, non-core assets, non-controlling interest (NCI) and debt equivalents can be included for a more detailed Enterprise to Equity Value Bridge. The additional elements are described below. This visual representation summarises the balance best:

Net Debt

Net debt is calculated as interest-bearing liabilities less highly liquid financial assets. Often this can be simplified to total debt (current and non-current) less cash and cash equivalents.

Non-Core Assets

Non-core assets are assets that are no longer considered necessary to a business’s core operation or are no longer used. This could include property, plant and equipment, natural resources, or investment securities, among other assets.

Debt Equivalents

Debt equivalents include any liability which could, through an event, be converted into debt. This includes debt-like claims e.g. capital and finance leases.

Non-Controlling Interest

Non-controlling interest (NCI), also called minority interest is the portion of a subsidiary company that is not owned by the parent company. This is typically less than 50% because if the portion is greater than 50%, the parent company usually ceases to be the controlling entity, and the company in question would no longer be a subsidiary of the parent.

Equity

This section of the calculation represents the equity value or the value attributable to the owners or shareholders of the business. It is found on a company’s balance sheet and consists of share capital, share premium, reserves and retained earnings or accumulated losses. It represents the amount of money that would be returned to the company’s shareholders if the company and its assets were liquidated and its debts paid off.

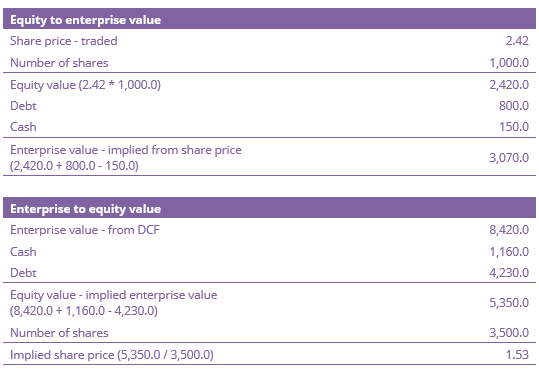

Example

A visual interpretation and a worked example of how to get from Equity Value to Enterprise Value and vice versa are shown below:

Limitations of Using Enterprise Value

As enterprise value uses debt in the calculation, it is important to contemplate how that debt is being used by the company. If the company is in an investment-intensive industry that uses a lot of capital, such as the construction industry, significant amounts of debt may be carried and used to buy machinery and promote growth. This could skew the enterprise value, so it is important when using it as a valuation tool to compare the company to similar companies in the same industry to get a better understanding of how the company is performing, and what its actual value is.